Deductible vs Out-of-Pocket Max

When selecting a health insurance plan, two key financial terms often cause confusion: deductibles and out-of-pocket maximums. While both impact how much you pay for medical expenses, they serve different purposes. Understanding these terms can help you choose a plan that aligns with your healthcare needs and budget.

What is a Deductible?

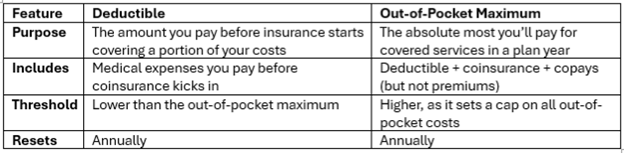

A deductible is the amount you must pay out of pocket for covered medical services before your insurance company begins to share the costs. Each year, you start with a fresh deductible, and only after you meet this amount does your insurance begin to cover a portion of your medical expenses.

How It Works:

If your plan has a $1,500 deductible, you must pay the first $1,500 in covered medical expenses before your insurance starts contributing.

Preventive services, such as annual checkups or vaccines, may be covered before you meet your deductible, depending on your plan.

After reaching your deductible, you’ll typically share costs with your insurance through copayments or coinsurance until you reach your out-of-pocket maximum.

What is an Out-of-Pocket Maximum?

The out-of-pocket maximum is the most you will have to pay for covered healthcare expenses in a plan year. Once you reach this limit, your insurance covers 100% of eligible medical expenses for the rest of the year.

How It Works:

Let’s say your plan has a $5,000 out-of-pocket maximum. Once you've spent $5,000 on deductibles, copays, and coinsurance, your insurance will fully cover additional eligible costs.

Monthly premiums do not count toward the out-of-pocket maximum.

Only in-network expenses typically apply; out-of-network costs may have a separate or unlimited out-of-pocket amount.

Key Differences Between Deductibles and Out-of-Pocket Maximums

Why It Matters

Understanding these two concepts helps you determine your total potential healthcare costs for the year. If you have frequent medical needs, selecting a plan with a lower deductible and reasonable out-of-pocket maximum may be beneficial. If you rarely visit the doctor, a higher deductible plan with lower premiums could save you money.

Final Thoughts

Choosing a health insurance plan requires balancing monthly premium costs with potential out-of-pocket expenses. By knowing the difference between deductibles and out-of-pocket maximums, you can make informed decisions that best suit your health and financial situation.

Still have questions? I’m here to help you navigate your options and find the right plan for you!

Kyra's Heath Insurance Solutions, LLC

kyra@kyrashealth.com

843-666-2840

© 2025 Kyra's Heath Insurance Solutions, LLC. All rights reserved.

I consent to receiving text messages from Kyra's Health Insurance Solutions, LLC. I have reviewed and agreed to the Terms of Service and the Privacy Policy. You can opt-out of messages at any time by texting STOP. Your carrier may charge you normal SMS or data rates.